Buying your first home in Scotland can feel daunting, especially as the Scottish property buying process works differently from the rest of the UK. From Home Reports and solicitor‑led offers to missives and legally binding contracts, knowing what happens and when can make all the difference.

This guide explains how to buy a home in Scotland step by step, so you can approach your purchase informed, prepared and confident.

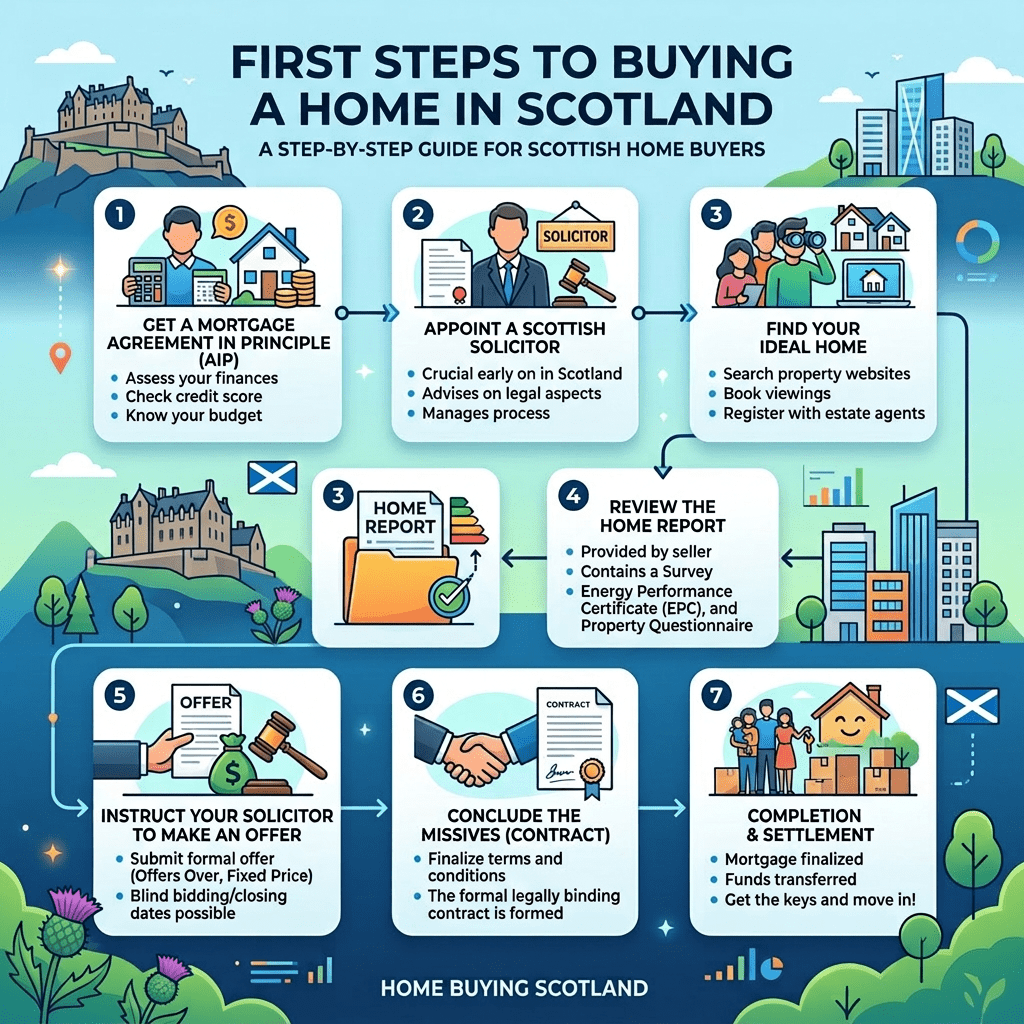

Step 1: Affordability Check

You’ve decided that you’re going to be buying your first home. Before you start viewing properties, it’s essential to understand what you can comfortably afford.

A mortgage broker like us will assess your income, outgoings, credit commitments and deposit to determine a realistic budget. This step helps prevent disappointment later and ensures your finances are sustainable long‑term.

Step 2: Decision in Principle (DIP)

A Decision in Principle (DIP) gives an indication of how much a lender may be willing to lend you. While it’s not a guaranteed mortgage offer, it shows sellers and solicitors that you’re a serious and credible buyer.

Some DIPs leave a footprint on your credit file, so it’s important to discuss this with your mortgage broker first.

Step 3: Choose a Solicitor

In Scotland, all property offers ideally must be submitted by a solicitor. Choosing one early is crucial.

Your mortgage broker can often recommend a trusted solicitor experienced in Scottish conveyancing. Your solicitor will handle the legal work, review the Home Report and submit offers on your behalf. They must also be approved by your chosen lender, another reason to speak to your mortgage broker about recommendations first.

Step 4: Make a Verbal Offer

Once you find a property you’d like to buy, your solicitor submits a verbal offer to the selling agent. This confirms your interest and proposed price but is not legally binding.

Step 5: Offer Accepted & Written Conditional Offer

If the seller accepts your verbal offer, your solicitor submits a formal written conditional offer. This is usually subject to:

- Receiving a satisfactory mortgage offer

- Acceptable valuation

- Any other agreed conditions

Unlike elsewhere in the UK, Scottish written offers can include timescales, so professional advice at this stage is essential.

Step 6: Mortgage Application

With an accepted offer in place, your mortgage adviser submits your full mortgage application.

You’ll typically need proof of income, recent bank statements and identification and the majority of mortgage brokers will have requested this at the DIP stage. The lender will begin their underwriting checks and review the property.

Step 7: Conveyancing Begins & Valuation

Conveyancing begins alongside your mortgage application. Most lenders rely on a transcript of the seller’s Home Report for valuation purposes, provided it’s up to date (dated in the last three months) and satisfactory.

If needed, you can arrange additional surveys for extra reassurance.

Step 8: Mortgage Offer Issued

Once the lender is satisfied with your application, affordability and valuation, they issue a formal mortgage offer. This confirms the loan amount, interest rate, term and conditions.

Your solicitor reviews the offer before progressing.

Step 9: Finalising Conveyancing & Insurances

Your solicitor finalises the remaining legal work and confirms the entry date with the seller’s solicitor.

At this point, you must also arrange buildings insurance, which is required before contracts are concluded. Other insurances such as life insurance and income protection ideally should be arranged and ready to go by this point.

Step 10: Conclusion of Missives

Once all terms are agreed, the missives are concluded. This is when the contract becomes legally binding in Scotland. After this point, neither party can withdraw without penalty.

Step 11: Completion & Moving In

On the agreed entry date, funds are transferred, keys are released and ownership changes hands.

Congratulations—you’re officially a homeowner and been successful in buying your first home.

Need help navigating the Scottish home‑buying process?

Munro Mortgages supports first‑time buyers across Scotland from affordability checks through to completion.

This article is for information only and does not constitute financial or mortgage advice. Your home may be repossessed if you do not keep up repayments on your mortgage. Munro Mortgages is a trading style of The Lending Channel, authorised and regulated by the Financial Conduct Authority (FCA), FCA number 626787.

Leave a Reply